FAIR PRACTICES CODE

1. Background

The Reserve Bank of India (RBI) has issued notification on Fair Practices Code for all Non-Banking Financial Companies (NBFCs) thereby setting standards for fair business and corporate practices while dealing with their customers. Pursuant to the Notification issued by the Reserve Bank of India by its Circular No. RBI/2006-07/138 DNBS (PD) CC No.80/03.10.042/2005-06 dated 28th September, 2006, Akasa Finance Limited (hereafter referred to as the “AFL”), company incorporated under the provisions of the Companies Act, 1956 and registered with the Reserve Bank of India (RBI) as Non-Systemically Important Non-Deposit Accepting or Holding Non-Banking Financial Company (“NBFC-Non-NDSI”) has formulated this Fair Practices Code to lay down the procedures and/or practices while dealing with their customers.

In pursuance of the applicable guidelines issued by the Reserve Bank of India from time to time, the Board of Directors of Akasa Finance Limited has adopted the following Fair Practices Code of the company.

2. Objectives of the Code

The Key objective of the Code

a) To ensure Fair Practices while dealing with the customers and promote good, fair and trustworthy practices by setting up minimum standards;

b) To ensure greater transparency enabling customers in having a better understanding of the product and taking informed decisions;

c) To ensure that clients are advised of the terms and conditions of products/ services provided in a comprehensive manner for their consideration prior to commitment of a transaction;

d) To monitor and administer client accounts in a fair and transparent manner consistent with the terms and conditions of the facility provided;

e) Recovery and enforcement, where necessary is conducted following due process of law.

f) To ensure compliance of applicable regulations prescribed by RBI relating to fair practices.

2. Objectives of the Code

The Key objective of the Code

a) To ensure Fair Practices while dealing with the customers and promote good, fair and trustworthy practices by setting up minimum standards;

b) To ensure greater transparency enabling customers in having a better understanding of the product and taking informed decisions;

c) To ensure that clients are advised of the terms and conditions of products/ services provided in a comprehensive manner for their consideration prior to commitment of a transaction;

d) To monitor and administer client accounts in a fair and transparent manner consistent with the terms and conditions of the facility provided;

e) Recovery and enforcement, where necessary is conducted following due process of law.

f) To ensure compliance of applicable regulations prescribed by RBI relating to fair practices.

3. Applicability of the Fair Practices Code

I. Application for Loans and their processing

a) Loan application forms should include necessary information which affects the interest of the borrower, so that a meaningful comparison with the terms and conditions offered by other NBFCs can be made and informed decision can be taken by the borrower. The loan application form shall indicate the documents required to be submitted with the application form.

b) The Company shall devise a system of giving acknowledgement for receipt of all loan applications. Preferably, the time frame within which loan applications will be disposed of should also be indicated in the acknowledgement.

c) The customer would be explained the processes involved till sanction and disbursement of loan and would be notified of timeframe within which all the processes will be completed ordinarily.

II. Loan appraisal and terms/conditions

a) The Company should convey in writing to the borrower by means of sanction letter or otherwise, the amount of loan sanctioned along with the terms and conditions including annualized rate of interest and method of application thereof and keeping the acceptance of these terms and conditions by the borrower on its record.

b) It is understood that in a few cases, borrowers at the time of sanction of loans are not fully aware of the terms and conditions of the loans including rate of interest, either because the NBFCs do not provide details of the same or the borrower has no time to look into detailed agreement.

c) Accordingly, it is understood that not furnishing a copy of the loan agreement or enclosures quoted in the loan agreement is an unfair practice and this could lead to disputes between the Company and the borrower with regard to the terms and conditions on which the loan is granted.

d) The Company shall, therefore, invariably furnish a copy of the loan agreement along with a copy each of all enclosures quoted in the loan agreement to all the borrowers at the time of sanction / disbursement of loans.

III. Disbursement of Loans including changes in terms and conditions

a) The Company should give notice to the borrower of any change in the terms and conditions including disbursement schedule, interest rates, service charges, prepayment charges etc. The Company should also ensure that changes in interest rates and charges are effected only prospectively. A suitable condition in this regard should be incorporated in the loan agreement.

b) Decision to recall / accelerate payment or performance under the agreement should be in consonance with the loan agreement.

c) The Company should release all securities on repayment of all dues or on realisation of the outstanding amount of loan subject to any legitimate right or lien for any other claim the Company may have against borrower. If such right of set off is to be exercised, the borrower shall be given notice about the same with full particulars about the remaining claims and the conditions under which the Company is entitled to retain the securities till the relevant claim is settled/paid.

IV. General Provisions

a) The Company should refrain from interference in the affairs of the borrower except for the purposes provided in the terms and conditions of the loan agreement (unless new information, not earlier disclosed by the borrower, has come to the notice of the lender).

b) In case of receipt of request from the borrower for transfer of borrowable account, the consent or otherwise i.e., objection of the Company, if any, should be conveyed within 21 days from the date of receipt of request. Such transfer shall be as per transparent contractual terms in consonance with law.

c) In the matter of recovery of loans, the Company should not resort to undue harassment viz. persistently bothering the borrowers at odd hours, use of muscle power for recovery of loans, etc.

d) The Company shall lay out appropriate internal principles and procedures in determining interest rates and processing and other charges.

e) The Company shall adopt an interest rate model taking into account relevant factors such as, cost of funds, margin and risk premium, etc and determine the rate of interest to be charged for loans and advances.

f) The rate of interest should be annualised rate so that the borrower is aware of the exact rates that would be charged to the account.

g) With particular reference to repossession of security/property (Movable or Immovable), the Company shall have a built-in re-possession clause in the contract/loan agreement with the borrower which must be legally enforceable. To ensure transparency, the terms and conditions of the contract/loan agreement should also contain provisions regarding: (i) notice period before taking possession; (ii) circumstances under which the notice period can be waived; (iii) the procedure for taking possession of the security/property (Movable or Immovable); (iv) a provision regarding final chance to be given to the borrower for repayment of loan before the sale / auction of the security/property (Movable or Immovable); (v) the procedure for giving repossession to the borrower and (vi) the procedure for sale / auction of the security/property (Movable or Immovable).

h) The Board of Directors of the Company shall review the Code and its implementation from time to time.

The Fair Practices code based on the guidelines outlined by RBI from time to time, shall be put up on the website of the Company for the information of various stakeholders.

V. Confidentiality

a) Unless authorized by the customer, Akasa Finance Limited shall treat all the personal information of its customers as private and confidential.

b) Akasa Finance Limited may not reveal transaction details of the borrowers to any other entity including within the group except under the following exceptional circumstances:

i. AFL has its duty to provide the information by statutory or regulatory laws including information to statutory bodies, law enforcement agencies, CIBIL, RBI and or other banks/financial institutions, any other state, central or any other regulatory body, including courts and tribunals having jurisdiction

ii. Customer has authorized AFL in writing, to provide such information

iii. If it is in the public interest to disclose such customer information.

iv. If its interest requires us to provide this information (e.g., Fraud prevention).

VI. Responsibility of Board of Directors of the Company

a) The Board of Directors of the Company shall lay down the appropriate grievance redressal mechanism within the organization comprising Business Heads, Heads of Risk and Collections and Heads of Operations to resolve disputes arising in this regard. This Forum will ensure that all the disputes arising out of the decisions the Company’s functionaries are heard and disposed of at least at the next higher level.

b) There will be a periodical review of the compliance of the Fair Practices Code and the functioning of the grievance’s redressal mechanism at various levels of management. A consolidated report of such reviews will be submitted to the Board at regular intervals.

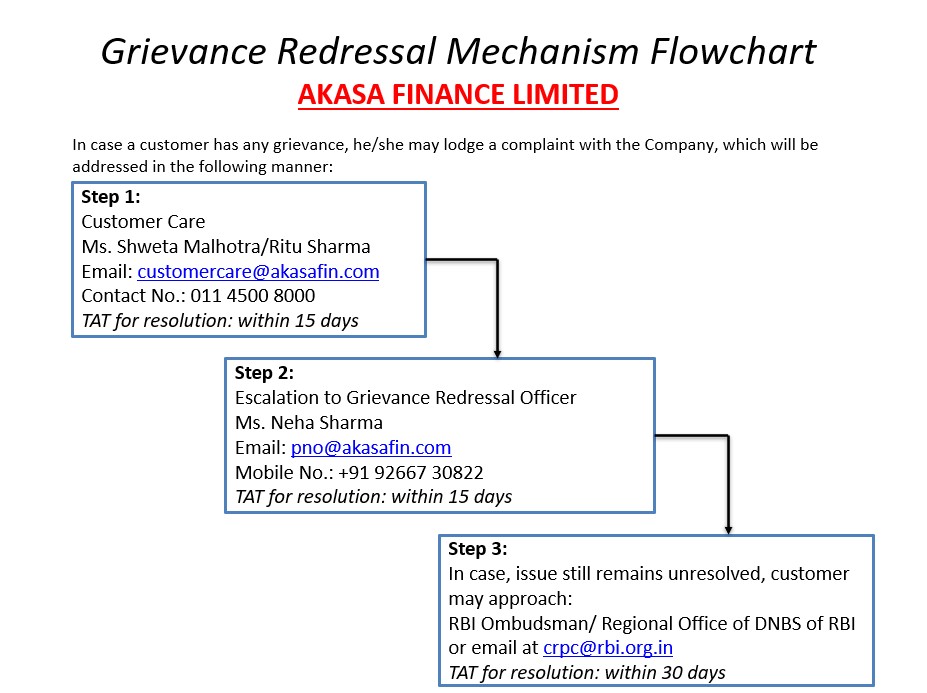

VII. Grievances Redressal Mechanism (GRM)

a) The Board of Directors of Company will also lay down the appropriate grievance redressal mechanism within the organization to resolve disputes arising in this regard. Such a mechanism should ensure that all disputes arising out of the decisions of lending institutions’ functionaries are heard and disposed of at least at the next higher level. The Board of Directors should also provide for periodical review of the compliance of the Fair Practices Code and the functioning of the grievance redressal mechanism at various levels of management. A consolidated report of such reviews shall be submitted to the Board at regular intervals, as may be prescribed by it.

b) A nodal officer and principal nodal officer shall be appointed for the redressal of the customer grievances including the borrowers, in connection with the any matter pertaining to business practices, lending decisions, credit management and recovery. The name and contact detail of both officers shall be displayed at the head office and every branch office of the company.

c) All communication in relation to the GRM shall be in writing.

In this regard, the company has also set up a dedicated e-mail address: customercare@pakasafin.com, where customers and other stakeholders including vendors can submit their grievances, complaints and suggestions. All complaints received by the Company shall be tabled at the meeting of the Board of Directors every quarter.

d) The name and contact details (telephone and email address) of the Grievance Redressal Officer (GRO) who can be approached by the public for resolution of complaints against the Company. The Company has appointed the following officials as Grievance Redressal Officer:

| Name of Grievance Redressal Officer (GRO) of the company | Neha Sharma |

| Contact No. | +91 9266730822 |

| Email Address | companysecretary@akasafin.com |

e) The name and contact details as mentioned below of Officer-in-Charge of the Regional Office (RO) of DNBS of RBI, under whose jurisdiction the registered office of the company Akasa Finance Limited falls, if the complaint is not resolved within prescribed time: –

| Name of Grievance Redressal Officer | General Manager Reserve Bank of India Department of Non-Banking Supervision 6, Parliament Street, New Delhi-110001 |

| Contact No. | 011-23714456 |

| Email Address | dnbsnewdelhi@rbi.org.in |

VIII. Language and mode of communicating Fair Practice Code

Fair Practices Code, preferably in the vernacular language or a language as understood by the borrower should be put up on the website of the Company for the information of various stakeholders. Copies will be made available on request.

IX. Regulation of excessive interest rates charged

Akasa Finance Limited will disclose to the borrower the risk and rationale for charging different rate of interest to different categories of borrowers in the application form and explicit communication in the sanction letter.

The rate of interest being charged by the Company shall be annualized rate to make the customer aware of the exact rates that would be charged to the account.

X. Complaints about excessive interest rates charged

Board of the Company shall lay out an interest rate policy mentioning internal principles and procedures in determining interest rates, processing charges and other charges.

XI. Clarification regarding repossession of vehicles financed

Akasa Finance Limited does not provide vehicle finance directly, but may do it through its intermediaries therefore, the following points as prescribed by RBI shall be followed:

(i) The Company will have an in-built re-possession clause in the loan agreement with the borrower which must be legally enforceable.

(ii) It will ensure transparency in the terms and conditions of the loan agreement regarding:

Notice period before taking possession

Circumstances under which notice period will be waived

Procedure for taking possession of security

A provision regarding final chance to be given to the borrower for repayment of loan before the sale/auction of the property

The procedure for giving repossession of the vehicle

Procedure for sale/auction of the property

(iii) It shall make sure that a copy of such terms and conditions is made available to the borrower in the loan agreement along with a copy each of all enclosures quoted in the loan agreement to all the borrowers at the time of sanction/disbursement of loans, which may form a key component of such contracts/loan agreements.

4. Review & Amendments

This policy shall be reviewed and updated periodically for any changes.

“In case any amendments issued by Reserve Bank of India in form of clarifications, circulars or guidelines or by any other name, which may not be consistent with the current provisions laid down under this Code, then the provisions of such amendments / clarifications, shall prevail upon the provisions contained in the RBI communication and the same shall stand amended accordingly effective from the date as laid down under such RBI communique.”

5. Disclosures

In compliance with the guidelines on ‘Fair Practices Code’, Akasa Finance Limited shall publish and disseminate the Fair Practices Code in English on the website of the Company and all the branches of the Company, and any borrower or client who wishes to obtain the same may request the AFL to provide it, thereof

{kind=link}